A digital bank helps position for a brighter future

April 13, 2020

Many industry analysts believe banks will survive the virus-induced storm and seize an optimistic, long-term view. The key now is prudent short-term expense management and long-term planning to take advantage of upcoming opportunities. Trends surfacing in the midst of the COVID-19 crisis indicate both the acceptance and wide-spread need for digital only, or direct banks, as we emerge from the current situation.

Three major factors that highlight the increased relevance of digital banks are the:

- Accelerated acceptance of digital only banking

- Anticipated need for liquidity

- Requirements for sound banking security

#1: Digital-only banking is accelerating

The importance of digital banking increases as consumers retain social distancing habits in their lifestyles. Consumers are becoming more inclined to conduct all their banking digitally. Key trends emerging from this crisis include:

- Branch decline: Social distancing is changing the way we interact personally and in business. More bank customers will become reluctant or unable to visit branch locations contributing to the decline of the branch channel.

- Cards with no physical interaction: The virus crisis will push consumers toward payment methods that require the least physical interaction. As a result, consumers may choose to pay with a contactless card or mobile wallet, since those do not require contact with point-of-sale terminals.

- Consumer hesitation regarding cash replenishment: Some individuals are now thinking about the risk ATMs or cash, particularly if used currency is loaded into cartridges.

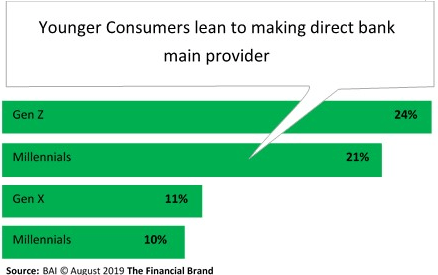

Some bankers still look at digital banks with a degree of scepticism. After all, they have always grown deposits through one-time promotions or new product offers. These old strategies don’t always work – as younger consumers favor direct or digital banks as their main provider of depository services. A recent article in The Financial Brand describes the increasing appeal of digital only financial institutions with Gen Z, Gen X and millennial consumers.

Looking beyond Gen Z and millennials, an underbanked population still exists within the U.S, and direct banks may offer an efficient means to service that market.

#2: The need for liquidity

Maintaining a strong balance sheet is always a priority for a bank, especially in the midst of a black swan event like the COVID-19 crisis. Banks with more liquidity will have more flexibility today and in a post-pandemic world. Additionally, the crisis could be creating pent up demand for refinancing based on declines in interest rates. If this does indeed come to pass, financial institutions would need new deposits to fuel refinancing growth as the world recovers from the crisis in the coming weeks and months. Initially, the loans made post-crisis will likely have very low interest rates, so inexpensive core deposits will be needed for banks to fuel new loan growth.

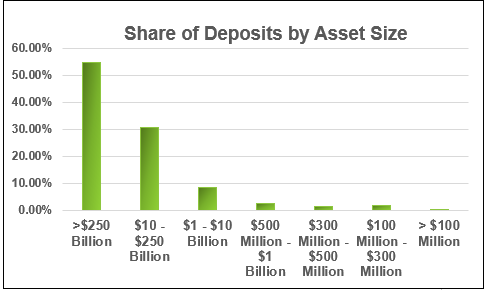

Longer term, smaller banks could face future liquidity challenges. Their share of total deposits continues to shrink when compared to global banks as shown in the most current data from the FDIC. Additional research from Darling and Associates suggests banks under $10 billion in assets have not grown core deposits sufficiently to fund loans for the past three years. The opportunity a digital bank offers to grow core deposits should not be lost on any institution, especially community banks.

#3: Robust security – a must

According to a recent article in Banking Strategies, “From the earliest days of the coronavirus outbreak, scam artists have worked to leverage the societal disruption – quarantines, service limitations, changing work situations – to steal money and information from banks and their customers.”

Digital banks must deliver services in a highly secure and reliable manner. Data breaches and ransomware attacks will continue to rise as fraudsters take advantage of the crisis. The recent hacking attacks illustrate the importance of resilient and secure technology delivery infrastructure provided with proven infrastructure within the financial services industry.

A digital bank’s foundation must rest on a highly secure foundation. As most financial institutions partner with technology providers to bring direct banks to market, they must fully vet the security of such integral collaborators.

A technology partner that adheres to a “Secure by Design” philosophy will provide their bank partners a platform that encompass application, network and device security to ensure bank customers receive a secure experience. The partner should provide proven infrastructure to help protect the institution’s investments in data, operations and reputational risk. The direct bank provider should also partner with leading industry experts, key governmental security and enforcement agencies to capture, analyze and assess threat intelligence. Doing so will help defend the bank and the bank partner from cyberattacks.

A Core on Demand approach addresses the renewed need for a digital only bank and exceptional security vigilance required in today’s world. This solution provides a path for completely digital banking presence, organic deposit growth that helps levels the playing field with large, global institutions and addresses security in a comprehensive holistic approach.

- Topics:

- Digital transformation

Similar Articles

It’s time for insurers to innovate and invest in insurtech

Innovation and digitalization in financial services

Driving asset finance growth with digital technology